Skip to content

Skip to content

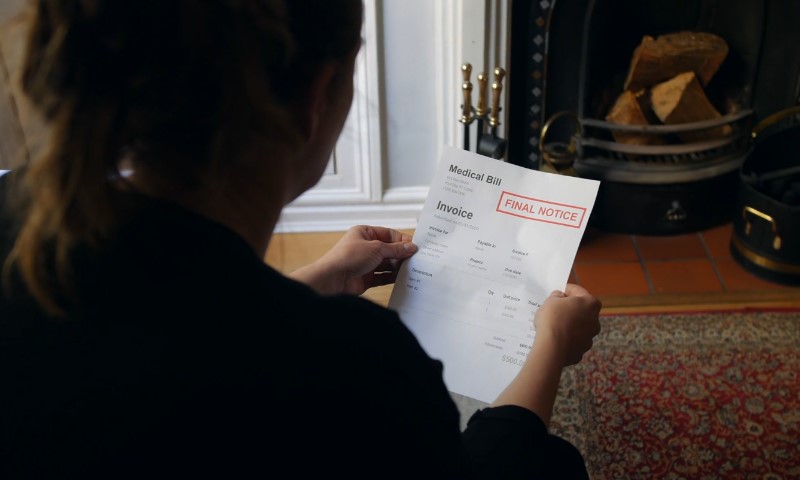

Medical debt is a fact of life for many Americans, and in Nevada, it has become the focus of one of the most consequential legislative debates of 2025.

Lawmakers in Carson City took up the question of whether medical bills should ever show up on a credit report, knowing that a single hospital stay can follow a person for years and reshape everything from mortgage applications to job offers.

Nevada’s Legislature advanced bold reforms in the form of two bills, AB204 and AB343, each aiming to change how medical debt is treated.

One sought a direct ban on reporting to credit bureaus, while the other linked debt collection to hospital price transparency. Together, they spotlighted Nevada as a test case in the absence of stable federal protections.

Key Points

- Nevada lawmakers debated two bills in 2025: AB204 (ban on reporting medical debt) and AB343 (tying collections to hospital price transparency).

- AB204 passed the Legislature but was vetoed by Governor Lombardo; AB343 moved forward with a focus on transparency.

- Medical debt affects about 7% of Nevadans, and many delay care or face bankruptcy because of it.

- Supporters argued the reforms would protect patients and promote fairness, while opponents warned of risks for lenders and hospitals.

Why Credit Reports and Medical Debt Collided in 2025

Credit scores are meant to reflect a person’s likelihood of repaying loans. They affect car loans, mortgages, rental applications, and even insurance premiums.

But medical bills are not traditional debts. They are rarely voluntary, often riddled with billing errors, and frequently subject to drawn-out insurance disputes.

When the CFPB finalized a rule in January 2025 to strip medical bills from credit reports nationwide, the move looked like a breakthrough. It would have removed about 49 billion dollars in medical tradelines, benefiting roughly 15 million Americans.

By spring, however, a federal court blocked the rule, and the CFPB retreated from defending it. That left states like Nevada facing a critical choice: either step in with their own protections or leave residents exposed.

Debt by the Numbers

The debate in Carson City was not abstract. Medical debt in Nevada is widespread:

- According to the Urban Institute, roughly 7 percent of Nevadans carry medical debt, which equals about 170,000 adults statewide.

- A 2025 poll found that over 40 percent of Nevada voters had delayed or skipped care because of debt.

- 14 percent reported filing for bankruptcy tied to medical bills.

Nationally, about 4.1 percent of consumers had medical collections on their credit records as of August 2024, or 9.7 million people. Nevada sits above that average, making the issue especially urgent.

Note: Residents facing accident injuries or hospital stays may also benefit from consulting a Las Vegas personal injury attorney to explore options for covering costs before they spiral into debt.

AB204

View this post on Instagram

AB204 became the centerpiece of Nevada’s 2025 debate, aiming to stop medical bills from ever appearing on credit reports.

Supporters pitched it as straightforward patient protection, while opponents warned of ripple effects for hospitals and lenders.

What the Bill Proposed

Assemblymember Max Carter introduced AB204 as a sweeping patient-protection measure. Its main features included:

- Ban on reporting: Health care providers and debt collectors would have been prohibited from reporting medical debt to credit bureaus.

- 180-day waiting period: No “extraordinary collection actions” such as garnishment or foreclosure until 180 days after the first bill.

- Limits on harsh tactics: Explicit restrictions on threatening arrest, filing liens on a primary residence, or foreclosing over unpaid medical debt.

- Effective date: Scheduled for late 2025 for new debts.

In essence, the bill would have erased medical debt from the list of tools creditors and collectors could use to pressure patients.

What Happened to AB204

The bill passed both legislative chambers, but Governor Joe Lombardo vetoed it on June 10, 2025.

The veto left Nevada without a full ban, even as neighboring states considered similar reforms.

The Governor’s message cited concerns about lender data access and potential unintended impacts on hospital collections.

AB343

Hospitals were already under pressure to show patients what care would cost, and AB343 pushed that idea further.

It tied medical debt collection to whether hospitals complied with transparency rules, adding a new layer of accountability to the system.

The Focus on Transparency

AB343 took a narrower but still significant route. It required hospitals to publish comprehensive price data, including:

- Detailed charge lists

- Consumer-friendly shoppable service lists

- Public disclosures on billing practices

Hospitals that failed to comply would be barred from collecting debts incurred during noncompliance.

Exhibits filed with legislative committees also referenced limiting reporting to credit bureaus, showing that transparency and reporting limits were intertwined.

Enforcement Tools

AB343 emphasized enforcement through:

- Public posting of violations

- Civil penalties

- Suspension of collection rights during periods of noncompliance

Why Medical Debt Is Different from Other Debt

Research consistently shows that medical debt is a weak predictor of credit risk. Studies highlighted in the CFPB’s rulemaking and by independent think tanks found:

- Billing errors are common: Insurance denials are often reversed, codes are misapplied, and patients are billed for out-of-network care they could not avoid.

- Debt is involuntary: Unlike credit card purchases or auto loans, medical bills result from emergencies or illness, not discretionary spending.

- Minimal impact on lenders: Removing medical debt from credit reports is expected to have little effect on lender default rates.

For many consumer advocates, keeping medical debt on credit reports amounts to punishing people for being sick.

Arguments in Nevada’s Debate

When the bills hit committee hearings, the conversation quickly split into two camps.

Supporters pointed to fairness and health equity, while opponents warned of data gaps and financial risks. Here’s how the arguments lined up.

Supporters’ View

Proponents of AB204 and AB343 highlighted:

- Fairness: Patients should not be penalized for emergencies or billing mistakes.

- Consumer protection: Keeping debt off reports prevents long-term harm to credit scores, affecting housing, employment, and insurance.

- Health equity: Medical debt hits hardest among low-income residents and communities of color.

- Simplification: Without credit reporting, disputes could be resolved through payment plans and financial assistance rather than coercion.

Opponents’ Concerns

Critics of the bills, including some hospital groups and trade associations, raised points such as:

- Data for lenders: Removing information could reduce transparency for banks and credit unions.

- Collections risk: Smaller or rural hospitals feared revenue shortfalls if patients had less incentive to pay.

- Patchwork rules: Some argued that medical debt regulation should remain federal to avoid a state-by-state patchwork.

Comparing Nevada to Other States

In 2025, several states considered or passed medical debt reforms:

- Virginia: Capped interest and wage garnishment for medical debts.

- California: Expanded hospital financial assistance rules.

- Wyoming and South Dakota: Similar bans failed under industry opposition.

What Blocking Medical Debt Reporting Would Mean in Practice

When lawmakers talk policy, it can sound abstract. But if Nevada were to block medical debt from credit reports, the ripple effects would land directly on patients, hospitals, collectors, and lenders. Here’s how the change would play out in real life.

For Consumers

- No medical tradelines on credit reports, removing a major source of score damage.

- More time to resolve errors with insurers during the 180-day window.

- Fewer catastrophic outcomes such as foreclosure or wage garnishment for medical bills.

For Hospitals

- Greater emphasis on transparency to maintain collection rights.

- Revenue cycle adjustments toward upfront estimates, financial assistance screening, and structured payment plans.

For Collectors and Bureaus

- Shift in strategy away from credit file leverage toward cooperative resolution.

- Loss of data feeds from Nevada, though research suggests minimal effect on overall credit risk accuracy.

For Lenders

- Little underwriting impact since medical debt is not a strong default predictor. Evidence shows traditional credit lines remain reliable signals.

Quick Comparison Table

| Policy Feature | AB204 (2025) | AB343 (2025) |

| Ban on reporting medical debt | Full prohibition | Referenced in exhibits, tied to transparency |

| Waiting period | 180 days | Debts barred while hospital noncompliant |

| Transparency rules | Not central | Core requirement: public pricing data |

| Status in 2025 | Passed Legislature, vetoed June 10 | Advanced, focused on transparency |

| Enforcement | Limits on garnishment, liens, foreclosure | Civil penalties, public posting of violations |

Practical Guidance for Nevadans Right Now

Even without AB204 in effect, residents can take steps to protect themselves:

- Check for errors: Request itemized bills and compare with your insurer’s Explanation of Benefits.

- Know your rights: Nevada law already requires a 60-day notification period before collections can be reported.

- Ask about financial assistance: Nonprofit hospitals must provide charity care policies. Request them in writing.

- Negotiate payment plans: Many providers will accept no-interest arrangements if you stay current.

- Monitor your credit reports: Use AnnualCreditReport.com to spot misreported debt and dispute inaccuracies.

Local resources like the Legal Aid Center of Southern Nevada, along with nonprofits such as Undue Medical Debt, can also provide support.

Where Nevada Stands and What’s Next

For now, the Legislature’s boldest proposal is off the table after the Governor’s veto of AB204.

AB343 remains a live track that links hospital transparency with collection rights. Federal protections are in limbo, leaving the issue largely to states.

Looking ahead, watch for:

- Reintroduction of a narrower bill, perhaps with compromises on reporting timelines.

- Transparency enforcement to see whether hospitals meet new disclosure requirements.

- Data tracking on whether Nevadans’ credit scores and access to loans change as state reforms unfold.

Closing Thoughts

The debate in Nevada showed how deeply medical debt touches everyday life. Lawmakers weighed whether someone’s emergency room bill should dictate their shot at a mortgage, a job, or a safe place to live.

AB204 did not survive, but it framed a conversation that will almost certainly return to Carson City.

The evidence points one way: blocking medical bills from credit reports would relieve a significant share of Nevadans without materially increasing lender risk.

Paired with transparency and fair billing, the change could make Nevada’s health care and financial systems fairer.

Until then, patients must work within the current patchwork of rights, resources, and protections to keep their health crises from becoming lifelong financial scars.