Skip to content

Skip to content

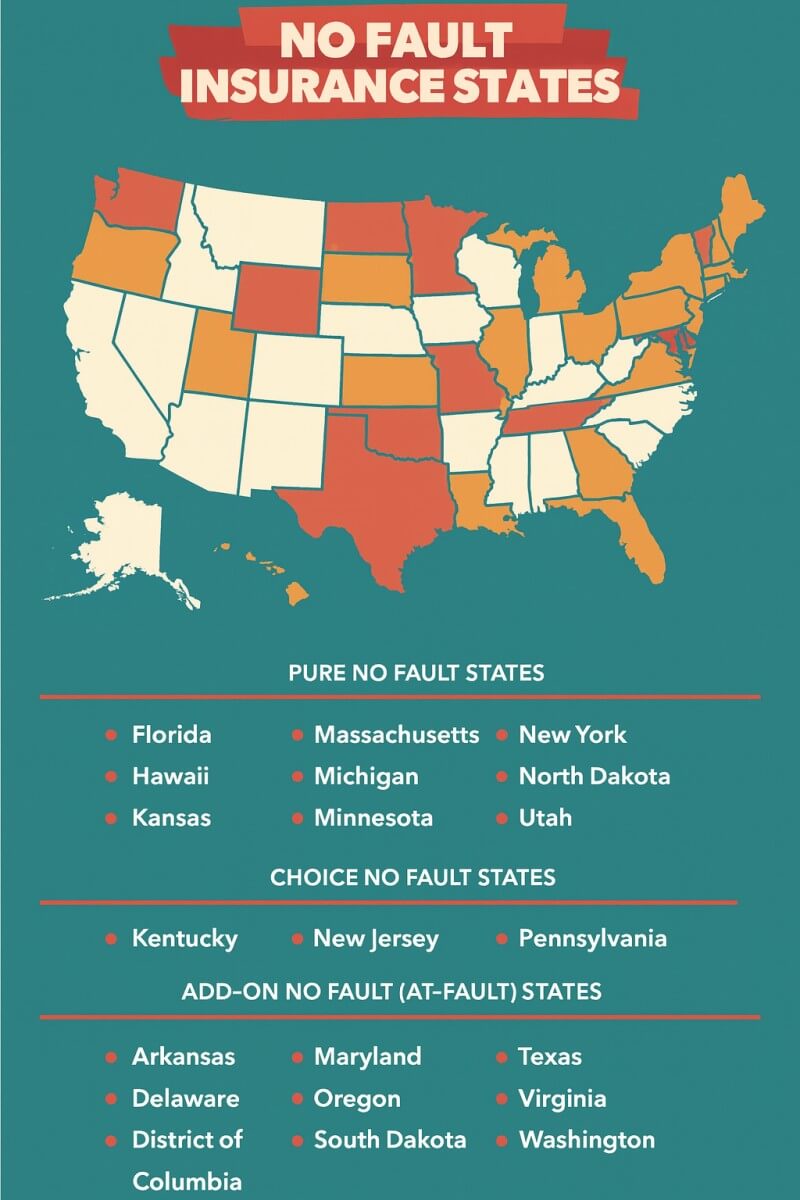

Car accident laws in the United States generally fall into two categories: no-fault and at-fault systems. The concrete answer is this: in 2025, only 12 states plus Puerto Rico still operate under some form of no-fault insurance law, while the rest of the country uses the at-fault (tort liability) system.

This difference matters because it determines who pays medical bills, how quickly drivers can access compensation, and whether lawsuits are allowed after a crash.

If you live in or drive through a no-fault state, your own insurance pays for injuries regardless of who caused the accident. In at-fault states, the driver found responsible (and their insurance company) pays for damages.

States With No-Fault Car Insurance in 2025

States With At-Fault (Tort) Systems in 2025

View this post on Instagram

The majority of U.S. states, 38 out of 50, operate under the at-fault (tort liability) system. In these states, the driver who causes an accident (or their insurance company) is financially responsible for damages. This includes medical expenses, lost wages, property damage, and compensation for pain and suffering. Unlike no-fault states, there is no strict threshold that limits lawsuits.

That openness gives injured parties broader access to the courts but also introduces higher stakes and more adversarial claims. In practice, many victims rely on legal counsel to navigate negotiations and potential litigation effectively, which you can check here. The absence of thresholds shifts the burden toward proof and strategy.

This system often leads to longer claims investigations because fault must be proven, but it gives injured drivers more freedom to sue for full compensation. Premiums in many at-fault states can be lower compared to no-fault states, although costs still vary widely depending on traffic density, accident rates, and state insurance regulations.

How No-Fault and At-Fault Laws Work in the U.S.

Car accident insurance systems in the U.S. fall into two main categories: no-fault and at-fault (tort liability). While both aim to protect drivers and ensure compensation, they function in very different ways and affect how quickly victims get paid, whether lawsuits are allowed, and how much people pay in premiums.

No-Fault States: How the System Works

In states with no-fault laws, each driver turns to their own insurance company for medical expenses and lost wages after an accident, regardless of who caused it. These laws were introduced in the 1970s to reduce the number of lawsuits clogging the courts and to make sure accident victims received money for treatment without long delays. Drivers in these states are required to carry Personal Injury Protection (PIP) coverage, which covers injuries up to a certain limit, according to Liberty Mutual.

- Medical and Wage Coverage – Your PIP policy pays for your medical bills and a portion of lost income after an accident, even if another driver was clearly at fault.

- Lawsuit Restrictions – To sue the at-fault driver for pain and suffering, you usually must meet a serious injury threshold, such as permanent disability, disfigurement, or medical expenses above a set dollar amount.

- Property Damage – Vehicle repairs are not covered by PIP. Instead, they follow the traditional at-fault model, meaning the negligent driver’s insurer pays for property damage.

- Premium Costs – Because insurance companies must pay out claims regardless of fault, premiums in no-fault states are often higher than in at-fault states. Florida and Michigan are well-known examples of states where drivers face some of the highest insurance rates in the nation.

Overall, no-fault systems provide faster payouts and guaranteed access to medical care, but they trade that convenience for higher costs and more limited legal options.

At-Fault States: How the System Works

In the majority of U.S. states, the at-fault system (also called the tort liability system) is the standard. Here, the person who caused the crash, or more precisely, their insurance company, is financially responsible for injuries, property damage, and lost wages. Unlike in no-fault states, lawsuits are not restricted by injury thresholds, which gives victims more legal leverage.

- Responsibility for Damages – The driver found to be at fault (or their insurer) pays for the other party’s medical costs, lost wages, and property damage.

- Lawsuit Rights – Victims can sue directly for compensation, including pain and suffering, without needing to prove a severe injury threshold.

- Claims Process – Because fault must be established, insurance investigations take more time, which can delay payments for medical care and income loss.

- Premium Costs – At-fault states sometimes offer lower insurance premiums compared to no-fault states, although costs vary widely depending on local accident rates, legal climates, and state regulations.

In states like Nevada, which follows the at-fault model, this distinction is especially important. Las Vegas consistently reports some of the highest traffic accident rates in the region due to tourism traffic, congestion on I-15, and a high percentage of pedestrian crashes along the Strip.

Because liability is key in these cases, many residents and visitors turn to advices from Accident Injury Lawyers such as Benson & Bingham for guidance on handling insurance disputes, injury claims, and understanding Nevada’s comparative negligence rules.

This highlights how the choice between no-fault and at-fault laws is not just theoretical; it shapes real outcomes for accident victims depending on where the crash occurs.

Bottom Line

If you drive in the U.S., knowing whether your state is no-fault or at-fault makes a big difference. In no-fault states, your own insurance pays for injuries first, and suing is harder. In at-fault states, responsibility falls on whoever caused the crash, and lawsuits are more common. For drivers, this impacts not just how claims are handled but also how much you pay for insurance every year.